Exit strategies for tenants are the part of a Slovak industrial lease that gets the least attention on signing day and the most attention three years later. A lease that runs its full term costs exactly what the rent schedule says; a lease that has to end early costs whatever the exit clauses allow – and under Slovak law, the statutory default allows very little. This article walks through the three routes out of a lease before its term ends – break options, assignment and subletting – what Act No. 116/1990 Coll. actually permits, and what occupiers should negotiate while the market still favours them.

Why exit flexibility is negotiated in good times

The paradox of exit rights is that they are cheapest exactly when they feel least necessary. Slovakia’s industrial market is currently generous to occupiers: CBRE’s first-quarter 2026 figures, reported by Property Forum, show total leasing of 136,000 square metres, up 47 per cent year on year, vacancy of 8.12 per cent across a modern stock of 4.87 million square metres, and prime rents around EUR 5.95 per square metre per month (Property Forum). In a tenant’s market, landlords compete on incentives – and flexibility is an incentive like any other, negotiable at the same table as the rent-free months and the fit-out budget. The problem the flexibility solves is a mismatch of horizons. Institutional leases in Slovakia commonly run five to ten years, while the supply chains inside them are redrawn far faster: nearshoring decisions, automation projects and customer wins or losses can double or halve a space requirement inside two years. Our review of warehouse lease terms in Slovakia shows how much of the contract is negotiable at signature; the industrial rent levels analysis shows what the headline figures hide. The same logic applies to leaving: the exit is drafted at entry, or it does not exist.

The statutory baseline: what Act No. 116/1990 actually allows

Slovak commercial leases live under two layers of law: the Civil Code, Act No. 40/1964 Coll. as the general regime, and Act No. 116/1990 Coll. on the lease and sublease of non-residential premises for anything used for business, commercial, administrative or storage purposes (CEE Legal Matters). The statute was built for stability, not flexibility. A fixed-term lease simply ends when the term expires; before that date, the landlord can terminate early only on a short list of enumerated grounds – the tenant using the premises contrary to the agreement, rent unpaid for more than one month, unauthorised subletting, or the building facing alteration or demolition, among others (DLA Piper REALWORLD). Where notice applies at all, the default period is three months, unless the parties agree otherwise. What the statute does not contain is any general right for a tenant to walk away from a fixed term because the business changed. There is no statutory break, no implied right to hand the lease onwards, and no consent standard a landlord must meet. Every usable exit route in a Slovak lease is therefore a creature of contract – which is precisely why the drafting matters more here than in jurisdictions whose statutes do more of the work.

Break options: flexibility you must write in

A break option is the cleanest exit: a contractual right to end the lease at a defined point before the term expires. Because the statute provides nothing of the kind, a break exists only if it is written into the lease – and its mechanics decide whether it is real or decorative. The anatomy is standard. Fixed break dates or a rolling window define when the right can be exercised; a notice period, measured in months rather than weeks, gives the landlord time to remarket; conditions precedent – no arrears, vacant possession, sometimes completed reinstatement – define what a valid exercise requires; and a break fee prices the landlord’s loss. That fee is not spite but arithmetic: incentives such as rent-free periods and fit-out contributions are amortised across the full term, and a tenant leaving at year five of ten walks away from half the period that was meant to pay them back. Occupiers should press for conditions that are objective and few – a break conditional on perfect compliance with every covenant is a break the landlord can usually defeat. And the timing interlocks with the handback: an underestimated reinstatement obligation can quietly disable a break that looked solid on paper.

Assignment and subletting: the consent gate

The second and third routes pass the space to someone else – entirely, by transferring the lease, or partially, by putting a subtenant underneath it. Here the statute speaks, and it speaks strictly. A tenant may sublet non-residential premises only with the landlord’s written consent and only for a limited period; subletting without consent is itself a statutory ground for the landlord to terminate the lease early (DLA Piper REALWORLD). A transfer is gated from the other side: under Slovak law a lease cannot be transferred unless the parties have agreed otherwise, so any change of tenant needs the landlord’s prior consent and cooperation (CMS), in practice documented in a trilateral agreement that also settles whether the outgoing tenant is released or stays on as guarantor. Crucially, the statutory default sets no standard for consent – no duty to be reasonable, no deadline, no obligation to give grounds. The discipline has to be negotiated: a carve-out for transfers within the corporate group, a consent standard with stated refusal grounds, a response period, and written consents that record the exit treatment of alterations. Institutional landlords process such requests routinely, but only the lease text turns their goodwill into an obligation.

Exit strategies for tenants in practice: the sublease market and the playbook

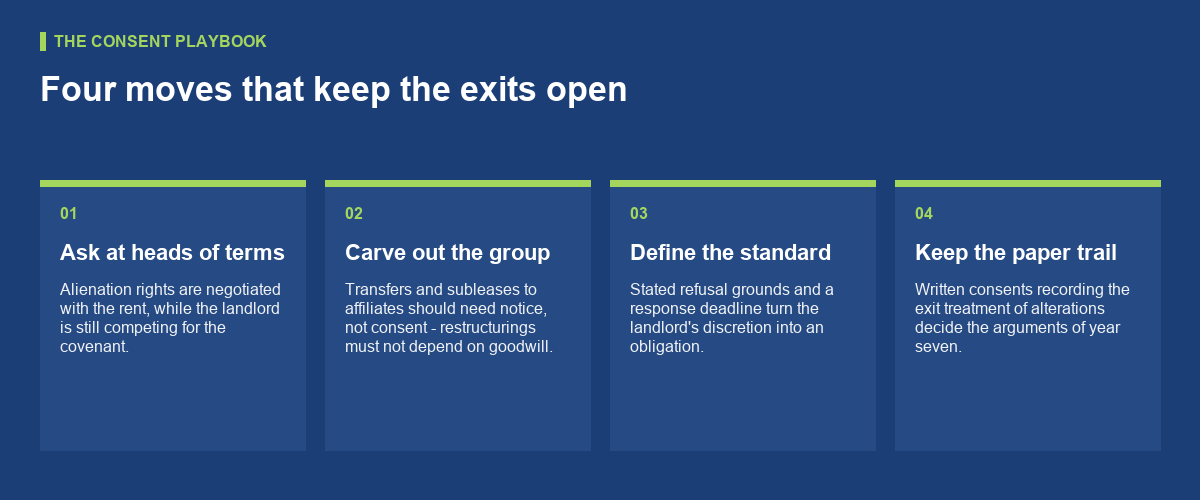

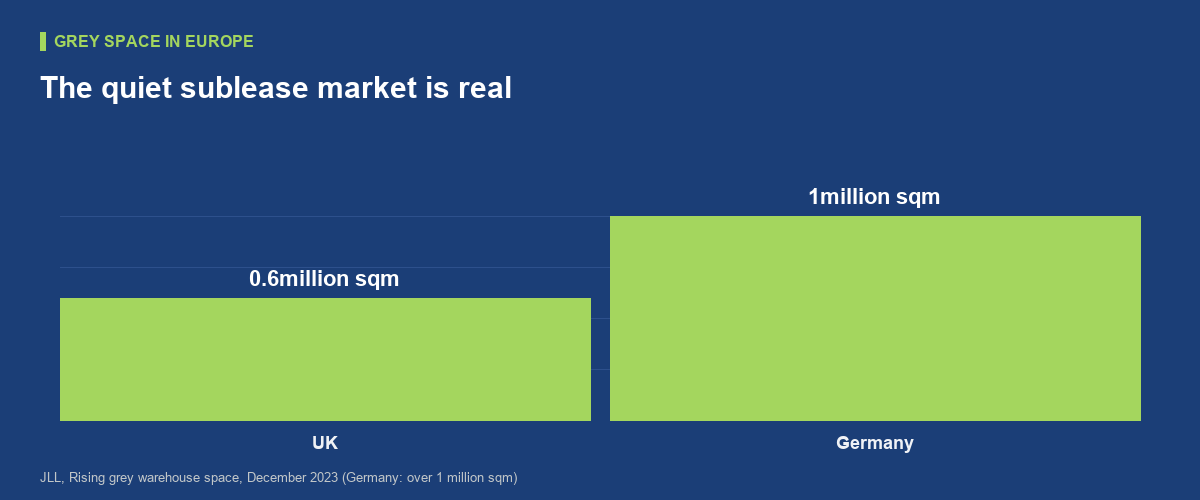

What do these routes deliver when space actually turns surplus? Europe’s quiet sublease market – grey space – gives the honest benchmark. JLL measured it at around 600,000 square metres in the UK and over 1 million square metres in Germany as of December 2023, noted that occupiers increasingly scan sublease availability before approaching the wider market, and judged that grey space is unlikely to move prime rental levels significantly (JLL). Slovakia’s version of that market is smaller and quieter still: surplus bays move through agents rather than portals, subleases rarely recover the full head rent, and a transfer usually needs a corporate event – an acquisition, a carve-out, a country exit – to supply the incoming tenant. The playbook for occupiers follows from everything above. Negotiate the break, the group carve-out and the consent standard at heads of terms, while the landlord is still competing for the covenant. Align the first break date with the amortisation of the incentives, so the fee conversation is short. Keep the paper trail – consents, condition records, alteration approvals – centralised from day one. And when surplus space appears, start the consent conversation with the landlord twelve months early: the tenant who asks in good time negotiates, the one who asks late pleads.

Conclusion

Slovak lease law gives occupiers stability and almost nothing else: fixed terms bind until expiry, subletting needs written consent, and a lease transfers only if the contract says so. Exit strategies for tenants are therefore drafted, not discovered – in the break clause, the alienation provisions and the consent standards agreed at signature. With vacancy above eight per cent and landlords competing hard for occupiers, 2026 is the moment to write those routes in. The lease you sign in a tenant’s market is the one you will have to live with when the market turns.