Cold storage in CEE is the strange corner of the logistics market where demand compounds every year and supply still barely moves. The region’s cold chain turns over more than twenty billion dollars annually, pharmaceutical flows are growing faster than any other application, and yet an occupier who needs 10,000 square metres of chilled space in Slovakia will find almost nothing standing empty – in a market whose overall vacancy sits above eight per cent. This article follows the money to explain the gap: what drives demand, why developers hesitate, what energy really costs, and how occupiers should respond in 2026.

The demand side: food, pharma and the compounding cold chain

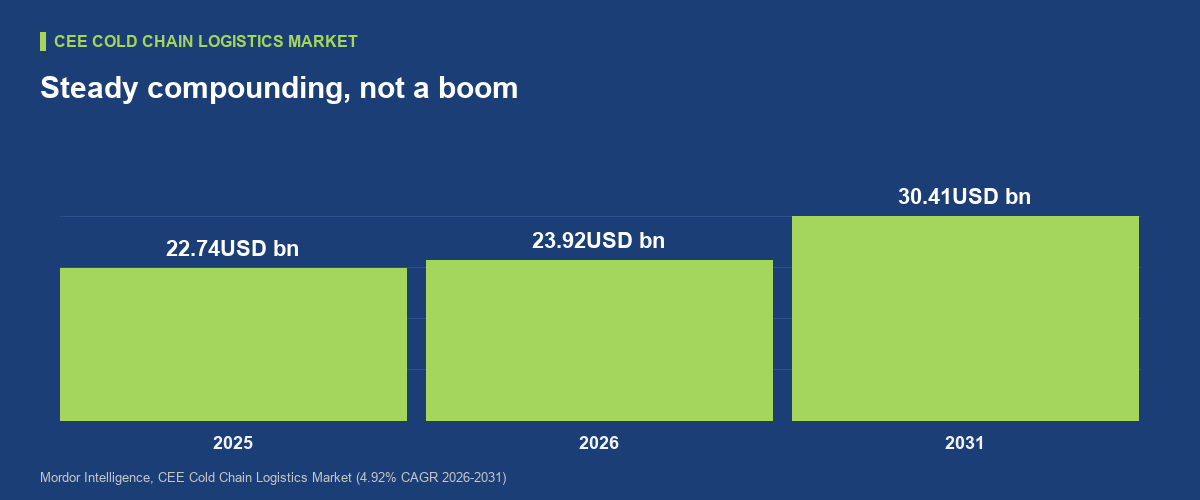

The demand numbers are not dramatic, and that is exactly their strength. Mordor Intelligence sizes the Central and Eastern European cold chain logistics market at USD 22.74 billion in 2025, rising to a projected USD 23.92 billion in 2026 and USD 30.41 billion by 2031, a compound rate of 4.92 per cent (Mordor Intelligence). Beneath the headline, the mix is shifting towards the expensive end. Chilled storage between zero and five degrees holds 45.1 per cent of revenue, but the frozen segment is accelerating at 6.11 per cent a year, and pharmaceuticals and biologics form the fastest-growing application of all at 6.73 per cent – flows that demand validated, documented, always-on cooling rather than a chilled corner of a dry hall. Geography tells the same story of catch-up: Romania leads the region with 33.72 per cent of revenue, while Poland grows fastest at 5.43 per cent a year. None of this is cyclical demand that arrives with a boom and leaves with a downturn. People eat, medicines need cold, and grocery supply chains keep consolidating – which is why cold chain revenue compounds through exactly the kind of soft leasing years that empty ordinary warehouses.

Why supply lags: the economics of building cold

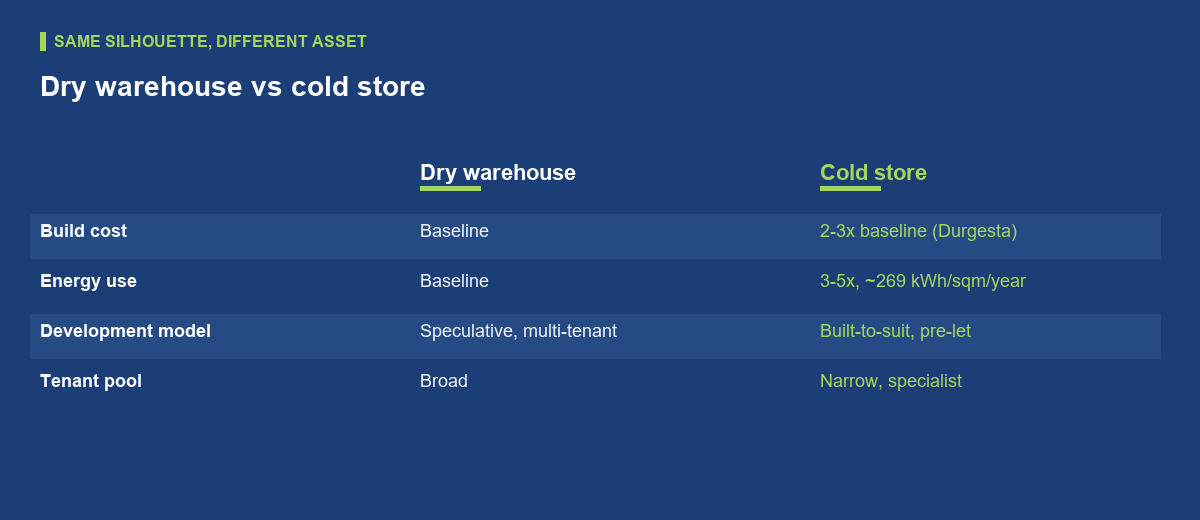

If demand is steady, why does supply not simply follow? Because a cold store is a different asset wearing a warehouse’s silhouette. Construction analysis by Durgesta puts the cold room itself at 110 to 235 euros per square metre depending on the temperature regime – fruit and vegetable rooms at the bottom, pharmaceutical and controlled-atmosphere rooms at the top – and a complete cold storage facility at 2 to 3 times the cost of a conventional warehouse (Durgesta). The premium buys insulated envelopes, refrigeration plant, reinforced slabs, vapour barriers and doors that behave like airlocks. That capital intensity breaks the speculative model the region’s logistics boom was built on. A developer who builds a standard hall can lease it to almost anyone; a developer who builds a minus-25 freezer store has narrowed the tenant pool to a handful of operators before the slab is poured. Worse, the fit-out is specific: the racking, the temperature zoning, the dock configuration all follow one user’s flows. So speculative cold space is almost never built, and nearly every new cold facility in CEE arrives as a built-to-suit with a pre-committed tenant and a lease long enough to amortise the plant.

Energy: the operating cost that shapes everything

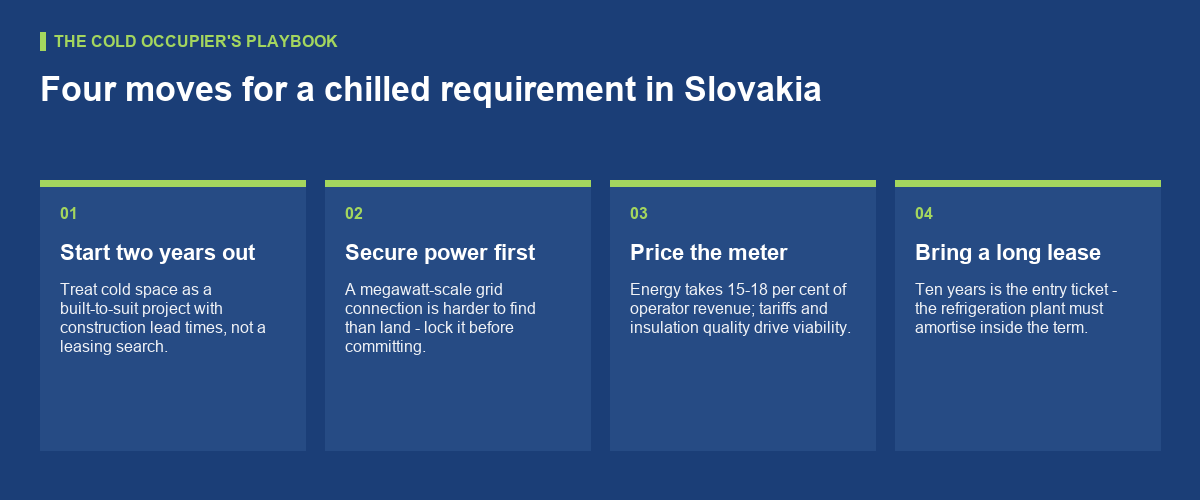

The second brake on supply is not the building but the meter. A cold store consumes about 269 kWh per square metre per year – roughly 3 to 5 times the energy of a conventional warehouse – and refrigeration alone accounts for 70 to 80 per cent of the electricity bill (Durgesta). Across the sector, energy absorbs an estimated 15 to 18 per cent of a cold operator’s revenue, which makes it the single largest operating expense and the line item that decides whether a facility is viable at all. For site selection the consequences are blunt. Power capacity at the plot matters more than the rent: a cold user needs a grid connection measured in megawatts, and in Slovakia grid capacity has already become a binding constraint on industrial development generally. Tariff structure matters almost as much, since refrigeration loads can flex into cheaper off-peak hours and thick insulation lets a well-run store ride through price peaks. And every euro per megawatt-hour of difference between two national grids quietly moves cold chain investment across borders, because no other warehouse type carries so much electricity in its cost base. Cheap land with a weak connection is, for this asset class, expensive land.

Cold storage in CEE and Europe: where capacity actually stands

Seen from the capacity statistics, Europe’s cold chain looks like a growth story, not a shortage. The Global Cold Chain Alliance’s 2026 Top 25 list puts the world’s largest operators at a combined 7.76 billion cubic feet, up 6.3 per cent in a year and 41.2 per cent since 2021 – and Europe’s top operators grew their capacity by about 90 per cent over six years, the fastest expansion of any region (GCCA). Both readings are true at once, and the reconciliation matters. The growth comes off a low base, it is concentrated in the hands of a consolidating group of specialist operators, and much of it lands in western European gateway markets rather than in CEE. Capacity is also not fungible the way dry space is: a chilled meat facility in Rotterdam does nothing for a pharma distributor in Kosice. So the region can post the fastest capacity growth in the world and still leave a mid-sized occupier in Slovakia without a single standing chilled option on the shortlist. Growth is real; availability is local, specific and mostly pre-let before construction starts. That distinction is the whole cold storage market in one sentence.

What the gap means in Slovakia: occupiers and developers

Slovakia illustrates the mismatch precisely because its dry market is currently comfortable. CBRE’s first-quarter 2026 figures, reported by Property Forum, show total leasing of 136,000 square metres, up 47 per cent year on year, overall vacancy of 8.12 per cent across a modern stock of 4.87 million square metres, and prime rents around EUR 5.95 per square metre per month (Property Forum). An occupier of dry space negotiates from strength. An occupier of cold space does not: the vacancy that matters to them rounds to zero, and in eastern Slovakia even general vacancy sits at just 2.66 per cent. The practical playbook follows from the economics. Occupiers should treat cold requirements as build-to-suit projects with two-year lead times, secure the power connection before the land, and expect leases long enough to carry the plant – ten years is the entry ticket, not a concession. Developers holding well-connected plots near food production, pharma manufacturing or grocery distribution hubs are sitting on scarce raw material: the industrial rent levels of dry space no longer describe what a committed cold tenant will pay for the right site. The gap between capacity and demand is not closing quickly – and for both sides of the deal, that is the opportunity.

Conclusion

Cold storage in CEE lags demand for reasons that are structural, not cyclical: a building that costs 2 to 3 times its dry neighbour, an energy bill that claims up to 18 per cent of revenue, and a speculative development model that cannot carry either. Demand, meanwhile, compounds quietly through food, frozen and pharmaceutical flows that do not care where the leasing cycle stands. For occupiers the lesson is to start early, buy power before space, and treat the lease as project finance. For developers and investors it is that the scarcest asset in the region’s logistics market is not another hall on the D1 – it is a grid-connected plot where cold can actually be built.