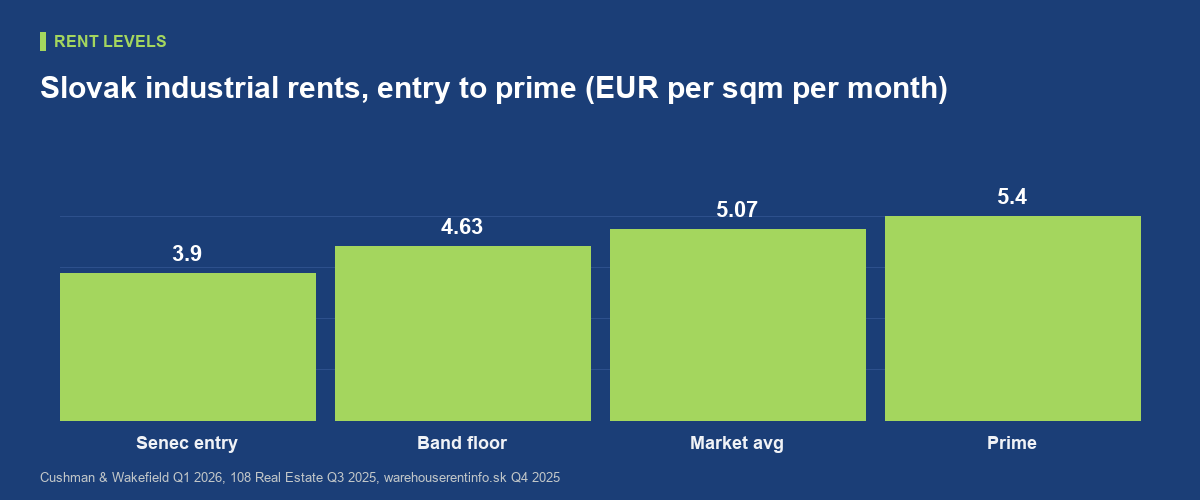

Industrial rent levels in Slovakia enter 2026 with a prime headline of 5.30 euros per square metre per month, the figure Cushman & Wakefield report for the first quarter. That single number hides a wide spread. The market average sits nearer 5.07 euros, entry rents around Senec start at 3.90 euros, and the gap between the headline and the effective deal has rarely been wider. This article sets out what occupiers actually pay across Bratislava and the regions, what service charges add on top, which incentives are realistic, how indexation works, and what all of it means for a lease negotiation on the D1 corridor this year.

Industrial rent levels in Slovakia: the 2026 headline numbers

Start with the numbers every negotiation quotes. Cushman & Wakefield’s Slovakia MarketBeat puts prime industrial rent at 5.30 euros per square metre per month in the first quarter of 2026, easing from 5.50 euros in mid-2025 (Cushman & Wakefield). Reviews of the fourth quarter of 2025 still held prime at 5.40 euros, with the average headline rent at 5.07 euros (warehouserentinfo.sk), and 108 Real Estate’s third-quarter report put typical rents between 4.63 and 5.22 euros (Property Forum, 108 Real Estate). Three things follow. First, prime describes a handful of the best units in the best parks around Bratislava, not the market; most occupiers should budget from the average band. Second, the average deal signs well below the prime print, and the distance between the two has widened as vacant space has accumulated. Third, the research houses no longer agree on direction: one prints a falling prime, another a flat one. When the data providers disagree, the market is moving, and everything else in the dataset says it is moving the tenant’s way. The honest anchor for a standard grade-A unit in the west is the band, not the headline. Where a unit lands inside that band depends on age, clear height, power supply and how long it has stood empty, and the last of those is the tenant’s information advantage.

Bratislava versus the regions: where the spread opens up

Slovakia holds about 4.67 million square metres of modern A-class industrial stock, and most of it stands in the west (Property Forum). Bratislava and the Senec node on the D1 set the top of the pricing curve, yet Senec is also where entry rents start lowest: units there have been offered from 3.90 euros per square metre per month, because that is where ready-to-occupy vacant space runs deepest (warehouserentinfo.sk). Across selected locations in the wider market, asking rents of 4.00 to 4.50 euros were typical through 2025 (Q2 2025 market review). The automotive belt of Trnava, Nitra and Zilina prices between those poles, anchored by plant supply chains rather than broad distribution demand, while Trnava and Senec are the two sub-markets where analysts expect further incentive offerings and rent reductions (108 Real Estate). Kosice and the east remain a thinner market: institutional stock is limited and pricing is set deal by deal rather than by a deep leasing market. The practical lesson is that the regional discount is really an availability discount. Rents fall where empty space concentrates, and right now that is the D1 corridor west of the capital, the spine we describe in Cross-Border Logistics Slovakia: CEE’s Pivot Point.

Service charges: the cost that sits on top of the rent

A headline rent is not the cost of occupation. Slovak industrial leases are typically structured as a triple net lease: the tenant pays the base rent, a service charge on top, and its own metered utilities. The service charge funds common-area maintenance, security, landscaping, snow clearing, building insurance and, in many parks, a property tax pass-through, billed as a monthly advance and reconciled once a year against actual costs. Two practical warnings follow. First, no two parks define the charge identically, so two identical headline rents can produce different total occupancy costs; ask for the last full-year reconciliation before comparing offers, not just the current advance. Second, the priced-separately components add up quickly. Integrated office space inside a warehouse unit was quoted at 9.00 to 11.00 euros per square metre per month in 2025, roughly double the warehouse rate, so an occupier fitting a ten per cent office share carries a visibly higher blended rent (Q2 2025 market review). On a five-year term those line items move the true cost per square metre further than the last ten cents of headline rent ever will, so a serious offer comparison carries every column, not the rent alone. Utilities sit outside both rent and service charge, and electricity capacity has become a negotiation of its own for automated operations, a constraint we set out in Industrial Power Capacity in Slovakia.

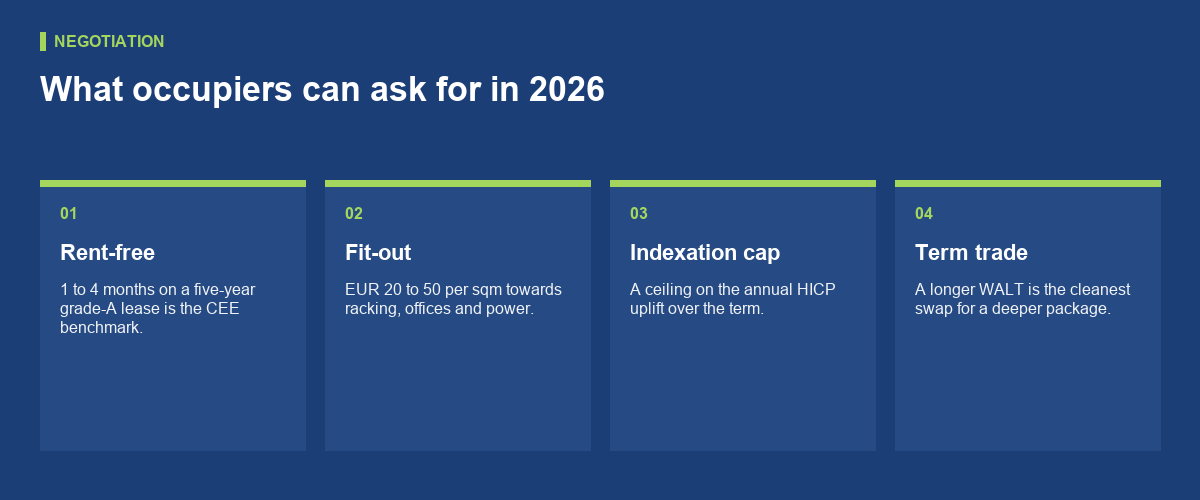

Incentives and indexation: the deal behind the headline

Incentives are where a soft market shows up first, because landlords protect the headline rent and give value away around it. The going CEE benchmark for a five-year grade-A lease is 1 to 4 months rent-free and a fit-out contribution of 20 to 50 euros per square metre, with larger requirements and longer commitments securing better packages (2026 CEE leasing guide). Slovak landlords are inside that range now: analysts tracking Trnava and Senec anticipate further incentives and rent reductions as speculative space completes (108 Real Estate). The arithmetic matters, because three rent-free months on a five-year term cut the effective rent by five per cent before any fit-out money is counted. Indexation is the other quiet lever. Euro-denominated CEE leases typically index annually to the harmonised index of consumer prices (Cushman & Wakefield), and euro-area inflation averaged 2.1 per cent in 2025 (Eurostat). That looks benign after the spike of 2022 and 2023, but uncapped indexation compounds over a term, so a ceiling on the annual uplift is a legitimate ask. Remember what the landlord wants in return: term. A longer commitment lengthens WALT, the income-security measure investors price, and it is the cleanest thing to trade for a deeper package.

What this means for rent negotiations on the D1 in 2026

The backdrop is the strongest occupier position in years. Vacancy reached 7.72 per cent in the third quarter of 2025, its highest level in recent years, before a strong final quarter of leasing, 82,496 square metres of net take-up, trimmed it to 7.40 per cent (Property Forum, warehouserentinfo.sk). Supply has not stopped: 311,365 square metres were under construction at the last count, roughly half of it speculative (108 Real Estate). Demand exists but it is selective, and third-party logistics operators took 33 per cent of newly leased space in the final quarter (warehouserentinfo.sk). The negotiating playbook follows from that. Benchmark against the effective rent of recent deals, not the asking rent on the brochure. Put the whole structure on the table at once, rent-free months, fit-out, an indexation cap and break options, because a landlord who will not move on one lever will often move on another. Press hardest where vacancy is deepest, in the Senec and Trnava stretch of the D1. And move while the window is open: speculative completions are still delivering into thin demand through 2026, which is exactly the condition that makes landlords compete. A built-to-suit commitment, by contrast, still prices like a landlord’s product, because bespoke space is financed against your signature.

Conclusion

Industrial rent levels in Slovakia are best read in 2026 as a band, not a number: from 3.90 euros at the accessible end of Senec to a prime print of 5.30 to 5.40 euros depending on who is counting, with the typical western deal signing in between. The headline has barely moved; everything around it has. Service charges deserve scrutiny, incentives are back on the table, indexation can be capped, and landlords along the D1 are competing for credible tenants. Occupiers who price the full structure over the full term will sign better deals than the sticker suggests. That window will not stay open once the speculative pipeline is absorbed.