The Slovak automotive belt is the reason nearshoring is more than a slogan in Central Europe. It is the chain of car plants and suppliers that runs across the country, and in 2024 it built about 993,000 vehicles – the highest output per head of any nation on earth. Now that belt is shifting: a decade of production weighted to the west is extending east toward Kosice, pulled by a €1.2 billion Volvo plant and the broader move to bring supply chains closer to the markets they serve. This article maps where the capacity is going, and what it means for occupiers.

What the Slovak automotive belt actually is

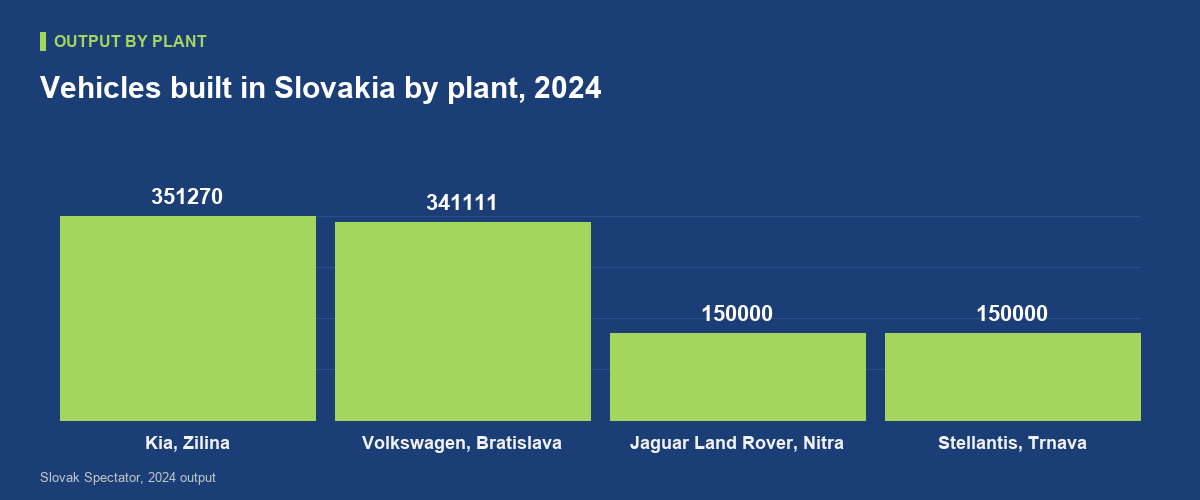

The Slovak automotive belt is the chain of car plants and their supplier networks that runs across the country, from Bratislava in the west toward Kosice in the east. Four carmakers anchor it today: Volkswagen in Bratislava, Stellantis in Trnava, Kia in Zilina and Jaguar Land Rover in Nitra. Together they built about 993,000 vehicles in 2024, which on a population of roughly five million works out at 182 cars per 1,000 inhabitants – the highest per-capita output of any country in the world, a position Slovakia has held since 2007 (Slovak Spectator; Wikipedia). This is not a side industry. Car and component manufacturing accounted for 49.5 per cent of total industrial revenues in 2023 and about 9.2 per cent of GDP, and the sector employs more than 165,000 people directly, or around 244,000 once the supply chain is counted (Slovak Spectator). The weight sits in a handful of plants: Kia in Zilina made 351,270 vehicles in 2024 and Volkswagen in Bratislava 341,111. When people say nearshoring is reshaping Central Europe, this belt is the physical thing the investment lands on.

Why nearshoring is redrawing the map

Nearshoring is the decision to move production closer to the market it serves, and after a decade of stretched, far-flung supply chains it has turned Central and Eastern Europe into Europe’s preferred factory floor. The drivers are practical: shorter transport routes, lower lead times, labour that still costs less than in Western Europe, and free movement of goods inside the EU (Cushman & Wakefield). For the car industry the pull is sharpened by the electric transition, which pushes carmakers to localise battery and component production rather than ship it across continents. Slovakia sits in the middle of this shift. It already has the plants, the trained workforce and the road and rail links along the D1, so new supplier investment tends to land where assembly capacity already is rather than starting from scratch elsewhere. That is the quiet logic of nearshoring: it concentrates, it does not scatter. Demand for space follows the same rule, which is why occupier interest in Slovak industrial property has stayed firm even though output dipped by about 90,000 units in 2024, from roughly 1,083,000 the year before. The belt is where the supply chain wants to be.

The eastward shift: Volvo and the Kosice axis

For most of its history the belt has been weighted to the west, around Bratislava and Trnava. That is changing. Volvo Cars is building a €1.2 billion assembly plant at Valaliky near Kosice, in the far east of the country, designed for 250,000 electric cars a year and at least 3,300 direct jobs, backed by €267 million of approved EU state aid (bne IntelliNews; electrive). Large-scale production has slipped to early 2027 (Mobility Portal), but the effect on the map is already visible. A plant of that size does not arrive alone: it pulls a ring of suppliers, logistics operators and service firms into a region that until now had little heavy automotive presence. For the first time the belt has a serious eastern anchor to match its western one, and the corridor between them – the spine we map in Cross-Border Logistics Slovakia: CEE’s Pivot Point – becomes the axis along which capacity, and property demand, will spread. Kosice is no longer the edge of the belt. It is becoming its second centre.

What the shift means for industrial occupiers

For anyone taking space in Slovakia, the nearshoring story is not an abstraction – it decides where the good buildings will be and what they will cost. Supplier operations that feed an assembly line need to sit close to it, so demand clusters tightly around the plants rather than spreading evenly. Around Bratislava, Trnava and Zilina that means a mature, competitive market where a tenant can compare standing buildings, a point we set out in The Slovak Industrial Property Market in 2026. Around Kosice it means something different: much of the specialised supplier space does not exist yet and will be built to order, the built-to-suit route we compare in Built-to-Suit vs Speculative Space in Slovakia. The practical read is to match your location to the plant you serve, and to move early in the east, where the pipeline is thin and the best sites near the Volvo plant will be committed well before production starts. Rent still matters, and we break down what occupiers actually pay in Industrial Rent Levels in Slovakia 2026, but in a belt this concentrated, position comes first.

The risks that could stall the belt

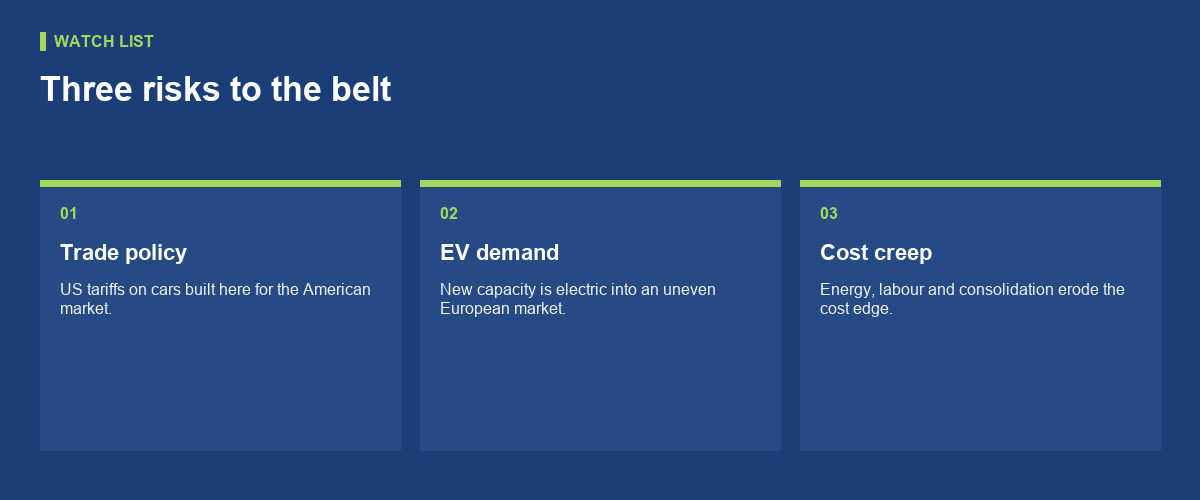

None of this is guaranteed, and honest planning means naming what could go wrong. The clearest risk is trade policy. A large share of Slovak output is exported, and cars built here for the American market – notably at Volkswagen and Jaguar Land Rover – are exposed to US tariffs, which would hit the plants and their suppliers together (Slovak Spectator). The second risk is the electric transition itself: Slovakia’s new capacity, Volvo included, is being built around electric vehicles at a time when European EV demand has been uneven, so a slower switch would leave expensive new lines underused. The third is closer to home. Rising energy and labour costs, sharpened by government consolidation measures, are eroding the cost advantage that drew the industry here in the first place (Slovak Spectator). None of these cancels the nearshoring case – the plants, the skills and the location are real and hard to replicate – but they do mean the belt will grow in fits rather than a straight line. Occupiers should plan for a strong long-term trend carried on a bumpy road.

Conclusion

The Slovak automotive belt is the clearest example in Central Europe of nearshoring turning into concrete and steel. It already produces more cars per head than anywhere on earth, it anchors close to half of the country’s industrial revenue, and it is now extending east toward Kosice on the back of Volvo’s €1.2 billion plant. For occupiers the message is simple: capacity is moving, it is moving in a predictable direction, and the best positions – especially in the east – will be taken by those who read the map early. The output dip of 2024 and the tariff and EV risks are real, but they change the pace of the story, not its direction. Match your location to the plant you serve, move ahead of the pipeline in the east, and the belt works for you rather than around you.