Warehouse automation used to be a question for the operations director; in 2026 it has become a question for whoever signs the lease. Robot fleets change what a building must be able to do – the flatness of its floor, the capacity of its slab and frame, the electrical headroom behind its meters – and they change it before the first tote moves. With Europe’s automation spend on course to more than double by 2031, occupiers across Central and Eastern Europe are discovering that the building specification, not the software, decides how far the business case carries. This article walks through what robotics actually change about the industrial building – and what that means in Slovakia’s occupier-friendly market.

The spending curve: Europe’s automation market is doubling

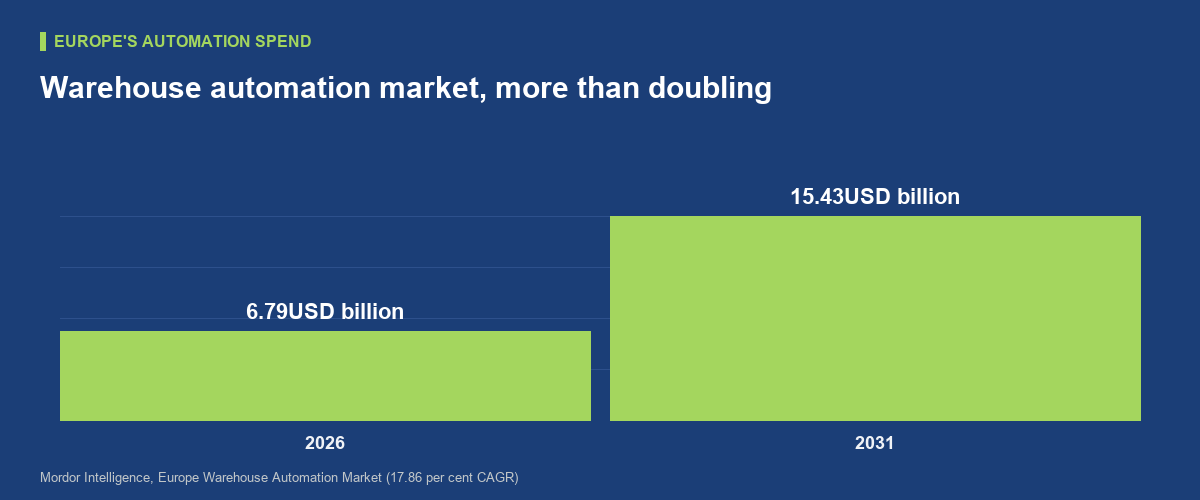

The direction of travel is not in dispute. Mordor Intelligence values Europe’s warehouse automation market at USD 6.79 billion in 2026 and forecasts USD 15.43 billion by 2031 – a 17.86 per cent compound annual growth rate (Mordor Intelligence). Germany alone accounted for 29.35 per cent of 2025 revenue, and the pattern across the continent is a west-to-east diffusion: the technology matures in the high-labour-cost markets and then follows the supply chains into CEE, where labour is scarcer every year and the buildings are newer. Two details in the data matter more for occupiers than the headline. First, e-commerce and grocery operators generated 32.45 per cent of 2025 revenue, but manufacturing is the fastest-growing end user at a forecast 19.15 per cent annual rate – and manufacturing is precisely what fills Slovak industrial parks. Second, sites below 10,000 square metres are the fastest-growing size class at 18.55 per cent a year, even though large sites above 40,000 square metres still carried 51.05 per cent of 2025 revenue. Automation is no longer a mega-shed phenomenon; it is spreading down the size curve into exactly the units most CEE occupiers actually lease.

Floors: the tolerance nobody sees until the robots arrive

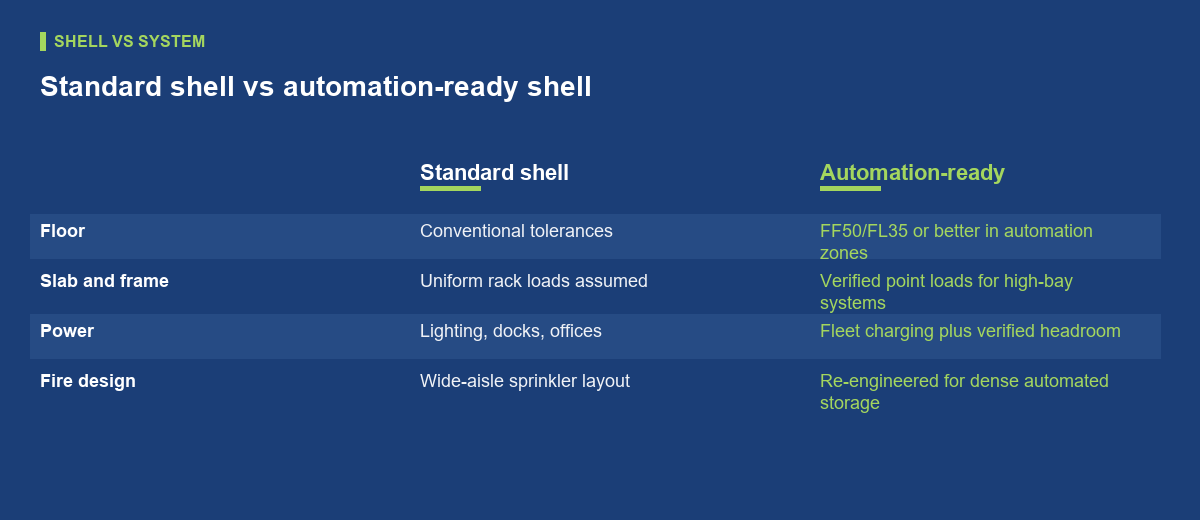

Every automated system stands, drives or racks on the same component: the slab. Autonomous mobile robots – at 36.20 per cent of the 2025 technology mix the largest single category in Europe (Mordor Intelligence) – navigate by sensors that assume the floor is a plane. It rarely is. Flooring specialists advise that automation zones should meet FF50/FL35 flatness and levelness tolerances or better, because slight waviness or elevation transitions between slabs can throw off sensors, cause vibrations and accelerate wear on drive components (Global Polishing Solutions). That is a materially tighter specification than a conventional shell assumes, and in Europe the conversation quickly reaches the measurement regime of DIN 18202 and, for very narrow aisle systems, defined-movement tolerances along the actual travel paths. The commercial point for occupiers: verify before you sign. A laser survey of the slab costs a fraction of what corrective grinding costs after the racking is up, and joints – where wheels cross a discontinuity thousands of times a day – deserve as much attention as the panels between them. High-bay storage adds the structural dimension: automated racking concentrates point loads the original slab design may never have contemplated.

The vertical consequences: height, structure and fire

Automation pushes buildings upwards. Shuttle systems and automated storage lift goods far higher than a reach truck comfortably works, which turns clear height from a nice-to-have into the variable that decides how much inventory a given footprint can hold. The consequences cascade through the structure. Taller, denser storage means heavier point loads into the slab and foundations; conveyor systems and sortation decks hang capacity demands into a roof structure that was sized for insulation and services; pick towers and mezzanine levels insert whole steel structures that need their own permits and their own fire engineering. Fire design is the discipline most often underestimated. Dense automated storage changes how a fire develops and how sprinklers must respond, and a system designed for wide-aisle pallet racking will usually need re-engineering – in-rack protection, revised head layouts, sometimes a different design standard altogether – before an insurer signs off an automated scheme. None of this is a reason to avoid automation; all of it is a reason to involve the landlord, the structural engineer and the insurer before the integrator finishes the layout. The building sets the ceiling, in both senses, on what the robots can deliver.

Power and data: the new utility question

A conventional warehouse draws power for lighting, dock doors and offices; an automated one adds a fleet that charges around the clock and control systems that must never brown out. Charging bays concentrate demand into short windows, peak loads rise, and suddenly the question is not the unit rate but whether the site connection has headroom at all – the constraint we examined in detail in our analysis of power capacity in Slovakia, where grid access has become a site-selection factor in its own right. Occupiers evaluating a building for automation should ask for the connected capacity, the reserved capacity and the upgrade path in writing, and treat a vague answer as a finding. Data infrastructure is the quieter sibling of the same issue: robot fleets coordinate over wireless networks that must cover every aisle, cold corner and mezzanine deck without dead zones, and the racking itself reshapes radio coverage as it fills. The practical consequence is cabling routes, antenna positions and server room space that belong in the fit-out design from day one – and in the consent conversation with the landlord, because punching cable trays through a roof deck retrospectively is exactly the kind of alteration that surfaces again in the reinstatement negotiation at exit.

What warehouse automation means for Slovak occupiers and landlords in 2026

Slovakia’s market is currently structured in the occupier’s favour, and that shapes the automation conversation. CBRE’s first-quarter 2026 figures, reported by Property Forum, show total leasing of 136,000 square metres, up 47 per cent year on year, net leasing of 59,000 square metres, up 35 per cent, and a vacancy rate of 8.12 per cent – up 31 basis points on the quarter – across a modern stock of 4.87 million square metres, with prime rents around EUR 5.95 per square metre per month (Property Forum). The regional spread is wide: 10.27 per cent in western Slovakia and 9.83 per cent in the centre, against 6.92 per cent around Bratislava and just 2.66 per cent in the east. For occupiers, empty space is negotiating power: renegotiations already make up 53 per cent of transactions and pre-leases another 26 per cent, which means landlords are competing hardest exactly where automation clauses are agreed – at renewal and at pre-lease. This is the moment to write the automation agenda into the lease: slab surveys and floor tolerances, verified power headroom, consent frameworks for mezzanines and roof penetrations, and realistic reinstatement language. Where requirements outgrow the standard shell, a built-to-suit project prices the specification honestly from the start – our review of industrial rent levels shows how wide the gap between headline and effective terms already runs. Landlords hold the mirror image of the argument: as new supply – approximately 83,000 square metres delivered in the first quarter alone – competes for tenants, an automation-ready specification is becoming the cleanest way to differentiate stock.

Conclusion

Warehouse automation is usually bought as technology and delivered as construction. The robots are the visible part; the decisive parts are a slab flat enough to navigate, a structure strong enough to load, a fire concept an insurer will sign, and a power connection with headroom. Occupiers in Slovakia negotiate all of that most cheaply now, while vacancy sits above eight per cent and landlords compete on flexibility. The specification you secure at signature – not the fleet you buy later – sets the limit on what automation can return.