Grid capacity has quietly overtaken land cost as the binding constraint on industrial site selection in Slovakia. A wave of EV and battery manufacturing investment — led by projects such as the Gotion-InoBat site in Šurany — is placing unprecedented MVA demand on a transmission network whose upgrade timelines are measured in years, not months. This article unpacks why industrial power capacity in Slovakia is now priced into land values before a single shovel breaks ground, what the SEPS coordination process actually means in practice for developers, and how the market is already sorting itself between sites that have secured capacity reservations and those that have not.

Why Industrial Power Capacity in Slovakia Has Become the Decisive Variable

For most of the past decade, site-selection decisions in Slovakia’s industrial corridors turned on three familiar variables: motorway proximity, labour cost, and land price. Power was an afterthought — a line item the utility would sort out within a few months of a planning application.

That assumption is no longer valid. New EV plants require roughly 60% more electricity than their conventional predecessors, and battery gigafactories operate at power intensities that would have been associated with smelters a generation ago. At the same time, Slovakia’s distribution zones are absorbing the cumulative load of a manufacturing boom that has added millions of square metres of modern industrial stock.

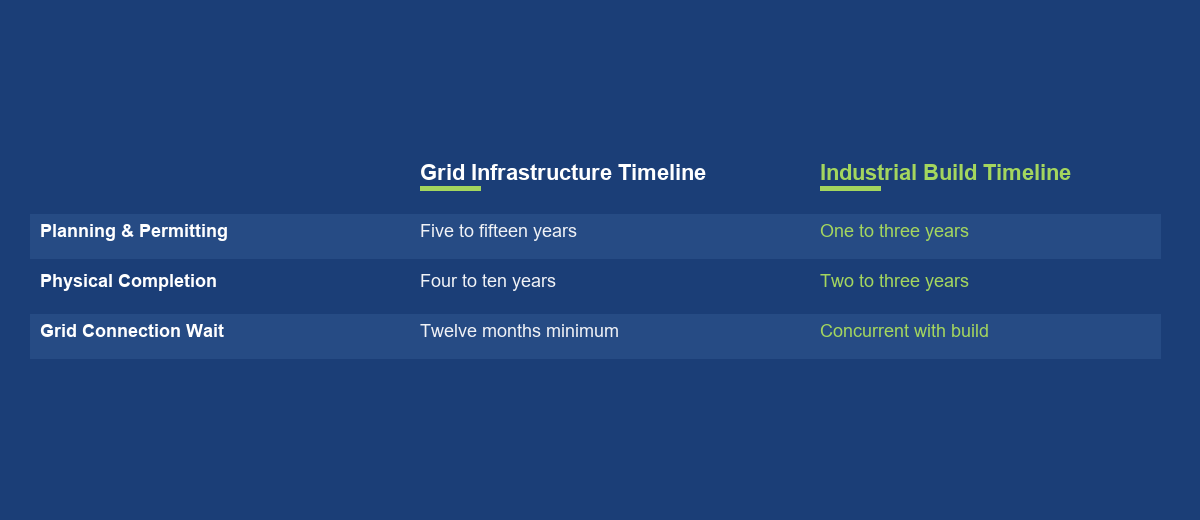

The structural problem is timing. According to the IEA’s Electricity 2026 report, planning, permitting, and completing new grid infrastructure can take anywhere from five to fifteen years — while the industrial facilities being built to connect to it are completed in one to three years. That gap is not a Slovak peculiarity; it is a Europe-wide misalignment. But Slovakia feels it acutely because the pace of new high-voltage demand arrivals — automotive, battery, and logistics combined — has compressed the queue on a grid that was not dimensioned for simultaneous greenfield mega-loads.

The result: power availability is now screened in the earliest phase of site feasibility, ahead of land tenure and labour catchment. Developers who cannot demonstrate a credible MVA reservation increasingly find that institutional tenants will not sign heads of terms, regardless of how competitive the rent or how direct the motorway access.

The SEPS Queue and What a Capacity Reservation Actually Costs

SEPS — Slovenská elektrizačná prenosová sústava — operates Slovakia’s high-voltage transmission backbone and is the first port of call for any industrial connection above distribution voltage. The practical reality facing developers is that a formal grid connection request triggers a multi-stage technical study process at SEPS and the relevant distribution system operator, with lead times that industry practitioners report stretching well beyond twelve months for larger loads before any physical work begins.

The European Commission’s December 2025 Guidance on efficient grid connections (C(2025) 8473) acknowledges the structural cause directly: “lack of physical grid capacity has been quoted as a prominent reason behind grid connection queues”, driven by the mismatch between infrastructure construction times of four to ten years and demand-side connection timelines of two to three years. As of mid-2025, at least 16 EU Member States face grid connection queues — Slovakia among them.

For developers, the financial implication is direct. Securing a capacity reservation requires early-stage capital commitment: connection studies, substation design fees, and in some cases co-financing of upstream grid reinforcement. Sites where a developer has already absorbed these costs — and holds a dated, documented MVA reservation — carry a structural premium over undeveloped plots nearby. The reservation is, in effect, a licensed monopoly on scarce infrastructure for the term of the agreement. Industrial plots with strong power infrastructure have seen values appreciate by 35–45% between 2023 and early 2026, a trajectory that reflects power scarcity as much as land scarcity.

The Transmission-Distribution Interface: Where Projects Stall

Most commentary on grid constraints focuses on the high-voltage transmission tier — the 400 kV and 220 kV lines managed by SEPS. The less-discussed bottleneck sits one level down: the 110 kV distribution interface, operated by the regional DSOs. This is where the majority of industrial connections physically land, and where technical study backlogs are most acute for loads in the 5–50 MVA range typical of logistics halls, automotive component plants, and mid-scale battery module assembly facilities.

A project that obtains a positive SEPS feasibility opinion can still stall at the DSO stage if the nearest 110/22 kV substation lacks available transformer capacity. Upgrading or extending that substation — a project the DSO must programme, permit, and fund — follows its own multi-year timeline. The EU’s broader grid investment picture signals the scale of the challenge: with 40% of Europe’s distribution grids over 40 years old, and EU electricity consumption expected to rise by around 60% by 2030, the investment requirement across the continent is estimated at €584 billion.

For Slovakia specifically, the IEA’s 2024 country review flagged that while some infrastructure bottlenecks have recently been removed, “more effort is needed to simplify, streamline and accelerate approval and permitting processes.” That is diplomatic language for a structural drag that developers operating on two-year build programmes cannot simply wait out.

The practical implication for site selection: proximity to a recently upgraded or over-built substation — one with headroom — is now a material differentiator in Slovakia’s industrial land market, on a par with motorway junction distance.

How Developers Are Pricing the Premium — and Who Gets Left Behind

A two-tier market is forming. On one side: industrial parks and build-to-suit plots where the developer has invested in early-stage grid engagement, secured a documented capacity reservation, and — in some cases — co-funded substation upgrades to create a site-wide power envelope that can be parcelled across multiple tenants. These sites command premium land values and shorter lease-up timelines because they remove the single greatest risk that a corporate occupier faces in Slovakia today: the risk of completing a building and then waiting twelve to twenty-four months for a grid connection.

On the other side: opportunistic land positions assembled without power due diligence. These may offer attractive headline prices, but sophisticated tenants — particularly automotive-tier suppliers and logistics operators running automated dark warehouses — are disqualifying them at the earliest stage of site scoring.

Slovakia’s industrial market added 4.6 million square metres of modern warehouse stock, but the distribution of viable power-ready sites within that stock is far from uniform. The Cushman & Wakefield H1 2025 CEE investment report confirms that industrial real estate accounted for 58% of total Slovak investment volume in H1 2025, with Slovakia’s investment volume reaching €536 million — a year-on-year increase of 315%. That capital is increasingly discriminating: acquirers and occupiers are underwriting power capacity alongside yield and lease term. Developers who cannot provide a clear answer to “how many MVA, reserved to when, and under what conditions” are losing mandates to those who can.

The build-to-suit segment is adapting fastest. Chinese investors — active in Slovakia’s battery corridor — frequently opt for build-to-suit deals rather than standard lease agreements, and their technical briefs now open with power specifications, not floor-plate dimensions.

Nuclear Baseload and the Medium-Term Outlook for Industrial Consumers

Slovakia’s power supply profile offers one structural advantage that developers should factor into medium-term positioning. Nuclear energy accounts for close to two-thirds of the country’s electricity generation, providing baseload reliability that markets with higher renewable penetration cannot match on a 24/7 basis. The Mochovce 3 unit — 471 MWe — reached successful completion in 2023. Mochovce 4, an additional 471 MWe unit, was expected to connect to the grid in 2025, adding meaningful national generation capacity.

For energy-intensive industrial tenants — battery module assembly, automotive painting lines, data-centre-adjacent logistics — baseload reliability and predictable off-peak pricing are operational requirements, not ESG talking points. Slovakia’s nuclear-weighted generation mix positions it ahead of coal-heavy peers in the region when corporate tenants are assessing long-run energy cost and carbon footprint under EU taxonomy frameworks.

The medium-term constraint, however, is not generation adequacy — it is transmission and distribution throughput. Slovakia’s overall electricity consumption is set to grow with the electrification of manufacturing, and delivering on energy and climate targets requires the timely expansion of robust transmission and distribution systems. Generation capacity alone cannot resolve a connection queue. The pipeline of grid reinforcement projects — and the permitting timelines attached to them — will determine whether Slovakia’s low-carbon generation advantage translates into a genuine competitive edge for industrial occupiers, or whether that advantage is stranded behind a congested interconnection queue.

Developers and investors watching this space should track SEPS’s ten-year network development plan alongside property fundamentals. The two documents, read together, tell the real story of where industrial power capacity in Slovakia will be available — and on what timeline.

Conclusion

Grid capacity has become the hidden yield driver in Slovakia’s industrial property market. Sites with documented MVA reservations command a structural premium; sites without them face tenant attrition regardless of location or specification quality. The asymmetry will widen as EV and battery manufacturing demand accelerates and the infrastructure gap — measured by the IEA in decades, not years — remains only partially closed. For institutional investors, developers, and corporate occupiers, the actionable implication is clear: power due diligence must begin at site origination, not at planning consent. The developers who understood this earliest are already pricing the new market. Contact IPEC Group to discuss how power capacity is assessed and secured in the site-selection process.