Cross-border logistics in Slovakia’s CEE position is no accident of geography, it is the product of three converging forces: the EU single market eliminating customs friction, a motorway spine that runs from Vienna to the Ukrainian border, and a national footprint small enough that a single distribution hall can reach four major industrial economies within one driver’s shift. According to Cushman & Wakefield’s H1 2025 CEE Investment Market Update, Slovakia posted a 315% year-on-year surge in commercial real estate investment volume, driven overwhelmingly by industrial transactions. This article unpacks why Germany, Austria, Hungary, and Poland are the demand engine, and why Slovakia is the operational answer.

Why Cross-Border Logistics in Slovakia Outperforms a Multi-Country Footprint

The conventional argument for Slovakia as a logistics hub starts with land cost. That argument misses the more durable structural advantage: operating from one Slovak location eliminates the compliance overhead of maintaining separate warehouse leases, labour contracts, and customs declarations across four jurisdictions.

Inside the EU single market, goods move without border checks, but a multi-country footprint still multiplies administrative touch-points: separate VAT registrations, differing national transport regulations, fragmented carrier contracts, and duplicated safety stock per country. Consolidating into one cross-border logistics node in Slovakia collapses those layers into a single operational entity.

The dwell-time argument is equally sharp. In a fragmented network, each national hub adds a load-unload cycle, a transit day, and a handoff between carriers. A centralised Slovak node serving Germany, Austria, Hungary, and Poland replaces four overnight line-haul legs with direct outbound routes, typically reducing total cycle time by one to two days on the DE-AT-HU-PL matrix. For manufacturers running just-in-time replenishment or e-commerce operators chasing next-day SLAs, that compression is material.

The investment market has noticed. According to Cushman & Wakefield, industrial and logistics properties account for up to 58% of total investment volume in Slovakia, the highest sectoral concentration in the CEE region. That skew reflects occupier demand, not speculative development: tenants selecting Slovakia are making an operational, not a financial, decision first.

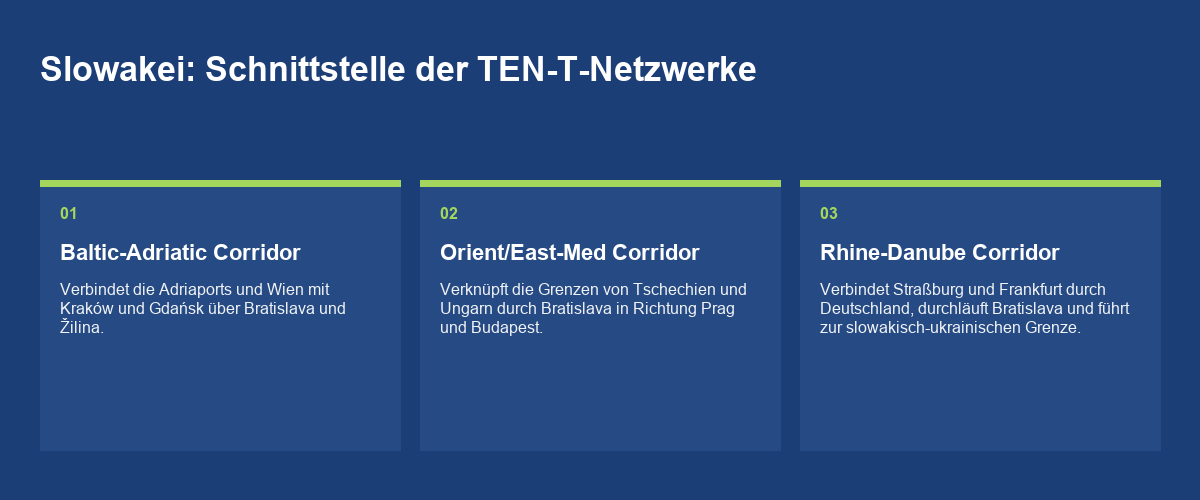

Three TEN-T Corridors Through One Country

Most logistics markets sit on one or two Trans-European Transport Network corridors. Slovakia sits on three, a structural fact that shapes every distribution network model operating in Central Europe.

The Baltic-Adriatic Corridor runs between the Austrian and Polish borders via Bratislava and Žilina, connecting the Adriatic ports and Vienna with Kraków and Gdańsk. The Orient/East-Med Corridor links the Czech and Hungarian borders through Bratislava, threading northward toward Prague and southward toward Budapest and the Balkans. The Rhine-Danube Corridor connects Strasbourg and Frankfurt through southern Germany, entering Slovakia via Vienna and continuing east toward Budapest, and, via a northern branch through Žilina, all the way to the Slovak-Ukrainian border.

As the European Commission confirms, more than 700 km of Slovakia’s rail network belongs to TEN-T Core Network Corridors, all converging on Bratislava. This is not a coincidence of route-planning; it reflects Slovakia’s position as the natural switching point between the Rhine-Main-Danube axis and the north-south Baltic-Adriatic spine.

For logistics operators, three overlapping corridors mean redundancy. If one route faces congestion or infrastructure works, alternative corridor capacity exists within the same national perimeter. That operational resilience is rarely priced into location decisions, but it should be.

The EU is investing heavily to maintain and expand this advantage. The CEF Transport programme for 2021–2027 carries a total budget of €25.8 billion, with Slovakia explicitly named among priority cohesion countries receiving rail and road upgrades.

Dwell Time, Customs Design, and the Hidden Cost of a Wrong Location

The cost competition in CEE logistics real estate tends to focus on headline rent per square metre. That framing obscures where the real money is lost: dwell time and customs processing, the hours or days a load sits stationary between origin and delivery.

Inside the EU customs union, Slovakia offers a frictionless transit environment for goods moving between Germany, Austria, Hungary, and Poland. There are no border formalities, no phytosanitary checks, no certificate-of-origin requirements for intra-EU freight. A truck departing Bratislava’s western fringe can reach Vienna in under an hour, Budapest in under two, and cross into Poland via the D1-D3 interchange at Žilina within three. That radius, four national markets, one fuel stop, is the operational logic behind the Slovak hub model.

The underappreciated design variable is yard configuration. A cross-border distribution hub handling four destination markets simultaneously needs sufficient dock capacity and maneuvering depth to run simultaneous inbound and outbound waves without creating yard congestion. Facilities that optimise for a single national market often lack the dock ratio and trailer parking depth to absorb multi-directional flows. This is the specification gap that separates a general-purpose warehouse from a genuine cross-border logistics node.

Customs-readiness is a secondary consideration for intra-EU flows, but matters immediately for any tenant handling third-country goods (UK post-Brexit, or goods originating in Asia or the Americas). Slovakia’s Customs Administration operates within the EU Customs Union framework, and proximity to Vienna International Airport adds air-freight inbound capability for time-sensitive components destined for onward road distribution across the DE-AT-HU-PL quadrant.

Companies evaluating sites should model total landed cost per pallet delivered, not rent per square metre. The differential frequently inverts the apparent cost advantage of a cheaper but less connected location.

Nearshoring Demand and the Structural Pull on Slovak Industrial Space

The supply chain disruptions of 2020–2022 triggered a structural reassessment of production geography across European corporates. The pattern that has emerged, nearshoring manufacturing and regional distribution closer to end-consumer markets, has created sustained occupier demand across CEE, with Slovakia positioned to absorb a disproportionate share.

Savills’ Autumn 2025 European Real Estate Logistics Census notes that occupiers are increasingly favouring CEE markets, whether for nearshoring purposes or as end-consumer markets in their own right, with the Czech Republic and Poland drawing the highest stated new-entrant interest. Slovakia sits downstream of that trend: it captures manufacturing and assembly operations that serve the same four-country distribution perimeter described above.

The automotive sector illustrates the dynamic most clearly. Slovakia hosts a disproportionately large automotive manufacturing base relative to its population. Component suppliers and finished-goods logistics operators serving those plants require cross-border inbound from German Tier-1 suppliers and cross-border outbound to Hungarian and Polish assembly lines, precisely the multi-directional flow that a centrally located Slovak hub handles efficiently.

Beyond automotive, Savills’ Q2 2025 European Logistics Outlook highlights that food and beverage, pharmaceutical, and defence-related manufacturing occupiers have been especially active across CEE. Each of those sectors carries temperature, security, or regulatory requirements that favour dedicated, purpose-built facilities over multi-tenant commodity space, and that preference aligns with the build-to-suit and design-build procurement models available at established Slovak logistics parks.

For institutional investors, nearshoring demand translates into longer lease terms and higher tenant covenant quality. That combination is driving the rerating of Slovak industrial assets visible in H1 2025 transaction volumes.

What Occupiers and Investors Should Scrutinise Before Signing

Slovakia’s structural case is compelling, but location within Slovakia matters as much as the country-level argument. The DE-AT-HU-PL distribution thesis works only if the facility sits on or near the D1 motorway corridor, where road access to all four markets is direct and uninterrupted.

Sites away from the D1, particularly in central or eastern Slovakia, add transit time toward Austria and Hungary that partially undermines the single-hub logic. A 90-minute detour to reach the Austrian border negates much of the dwell-time advantage described above. The D1 corridor around Bratislava and the Senec area represents the densest concentration of established logistics infrastructure in the country, with 3.1 million people accessible within 60 minutes and 6.4 million within 90 minutes, a catchment that spans both Slovakia and adjacent Austrian and Hungarian population centres.

Occupiers should also evaluate intermodal access. The Rhine-Danube and Orient/East-Med rail corridors converge on Bratislava, and intermodal terminals at Dunajská Streda and the wider Bratislava agglomeration provide rail-to-road transfer capability for high-volume flows. For operators running weekly block trains from German production sites, rail inbound combined with road outbound distribution is a material cost-reduction lever, but only if the facility is within practical docking distance of those terminals.

ESG compliance is the final variable that is reshaping location decisions. According to Savills’ Autumn 2025 Census, 88% of logistics occupiers now rate ESG regulation as an important factor in real estate decisions. Facilities that already carry BREEAM or DGNB certification, solar roof capacity, and EV charging infrastructure reduce the occupier’s own decarbonisation cost, and increasingly, that drives lease preference over marginal rent differences. The D1 Park Senec development land and adjacent Slovak logistics infrastructure are being designed with these specifications in mind.

Conclusion

Slovakia’s case for cross-border logistics in the CEE region rests on three interlocking pillars: EU customs-union frictionlessness, three converging TEN-T corridors, and road-time access to four major industrial economies within a single driver’s working day. The investment market has validated this thesis, Slovak industrial real estate recorded a 315% year-on-year investment surge in H1 2025, per Cushman & Wakefield, driven by occupiers making operational rather than purely financial decisions. For corporate real estate teams, site selectors, and institutional investors building logistics exposure in Central Europe, the key question is not whether Slovakia belongs in the network design, it is where within Slovakia, and with what specification, to extract the full distribution advantage.