The Evolution of European Logistics Real Estate: Market Analysis and Strategic Implications for 2026

Reflecting on the events of 2025, the European logistics real estate market unveiled a crucial phase, marked by investment volumes soaring to €16 billion in the year’s first half ↗. That’s a 6% uptick from earlier intervals. This leap points to a core reevaluation of how logistics spaces are appraised and engaged in our post-pandemic reality. However, these headline numbers only scratch the surface of a deeper market shift, one that is redefining location choice, asset management, and strategic foresight.

This metamorphosis holds significant weight as the European warehousing landscape speeds towards its forecasted worth of €661.21 billion by 2034, advancing at a compound yearly growth of 7.27% ↗. It’s about more than just the square meters or rental returns; it’s the dawn of a logistics era where location, tech, and sustainability integrate to forge competitive edges in unprecedented ways.

We dive into the lively market forces currently in play, scrutinizing how shifts in consumer habits, supply chain strategies, and tech advancements are birthing both hurdles and opportunities for those in logistics. Whether it’s the swell in city fulfillment hubs or the changes in cross-border networks, we’ll spotlight the main trends driving logistics real estate’s future.

By grasping these market movements, logistics professionals can better steer their way to triumph in a setting that’s only getting more complicated and fiercely competitive. Let’s break down the elements steering market change and their practical impacts on operators throughout Europe.

Market Dynamics and Growth Trajectories in Commercial Warehouse Space

The European logistics real estate sector put on an impressive show in 2025, featuring prime rents climbing by 4.4% year-on-year across 46 notable markets ↗. Though this rise has eased from previous peaks, it hints at a market maturely evolving rather than fading. With a modest vacancy rate of 4.4%, well below historical levels, the need remains robust despite economic challenges.

Western Europe’s key markets, particularly, stabilized early in 2025, seeing a slight 2% growth in leasing activity year-over-year in the first quarter. Still, this sits 21% shy of the decade average, leaving room for further recovery. Paris shines brightly, leading Europe with the highest take-up in industrial and logistics spaces over 12 months, highlighting the ongoing value of major urban hubs.

Investment behaviors expose a significant mood shift. During the first half of 2024, logistics real estate covered 22% of all European real estate investments—a record for the sector in a first-half segment, far above the 12.5% historic norm. This shift underscores investors’ escalating confidence in logistics as a foundational asset class.

Rent patterns paint a complex image between different market tiers. The European logistics realm now exhibits an estimated 10-15% rental potential, achievable by aligning existing leases with market conditions. This growth possibility not only counters inflation in many locales but offers a buffer against burgeoning costs. Yet, rental hikes vary widely based on location and asset quality.

As the market divides into premium and secondary assets, value-add prospects are cropping up. Top-tier warehouses are experiencing yield tightness, whereas secondary yields stay stagnant or experience slight expansion. This growing spread between primary and secondary yields offers fertile ground for astute investors to spot and revamp underperforming assets.

Strategic Location Considerations

In the rapidly evolving landscape of European logistics, choosing a location is no longer just about being close to transport hubs. Today’s operators weigh a web of factors such as workforce availability, power infrastructure, and last-mile delivery prowess. Facilities placed within a 500-kilometer orbit of major urban centers can cater to a staggering 45 million consumers—an essential metric in the era of lightning-fast deliveries.

Urban logistics sites are more vital than ever, with demand in city-adjacent areas growing 15% faster than in suburbs during 2025. This surge highlights the critical need for same-day shipping capabilities, with key European cities now setting delivery expectations that seemed outlandish a few years back. Paris, London, and Berlin are at the forefront of this urban logistics shift, commanding rental premiums of 25-40% over their suburban counterparts.

Changing cross-border shipping habits are redrawing location maps, particularly in Central and Eastern Europe. Data shows that centralized hubs serving several nations can slash operating expenses by up to 24% compared to country-specific setups. As a result, places like western Poland, eastern Czech Republic, and western Slovakia are in demand for their ability to serve multiple EU markets efficiently.

Power capabilities have emerged as a decisive factor, with facilities offering high electrical supply attracting higher rents. Research suggests that warehouses featuring greater than 2MW power connections see rent premiums ranging from 12% to 15% more than standard facilities, underscoring the rising use of automation and EV charging stations.

Labor supply is another critical factor affecting site selections, with companies leaning towards regions with robust workforce demographics. Areas abundant in skilled labor and offering competitive salary structures boast 18% higher occupancy rates over regions grappling with workforce scarcity.

Emerging Market Opportunities for Warehouse Development

Central and Eastern European territories continue to show promising prospects, with logistics investments rising by 32% in 2025 over 2024. Countries like Poland, Romania, and Hungary are leading this growth wave, buoyed by cheaper operational costs, up-to-date infrastructure, and strategic placements for pan-European distribution.

In these regions, yield premiums of 75 to 100 basis points above Western European markets are typical, yet these areas maintain comparable tenant quality and lease security. The development pipeline in these logistics hotspots remains measured, with fresh supply accounting for merely 3.8% of the existing inventory, laying the groundwork for enduring rental growth prospects.

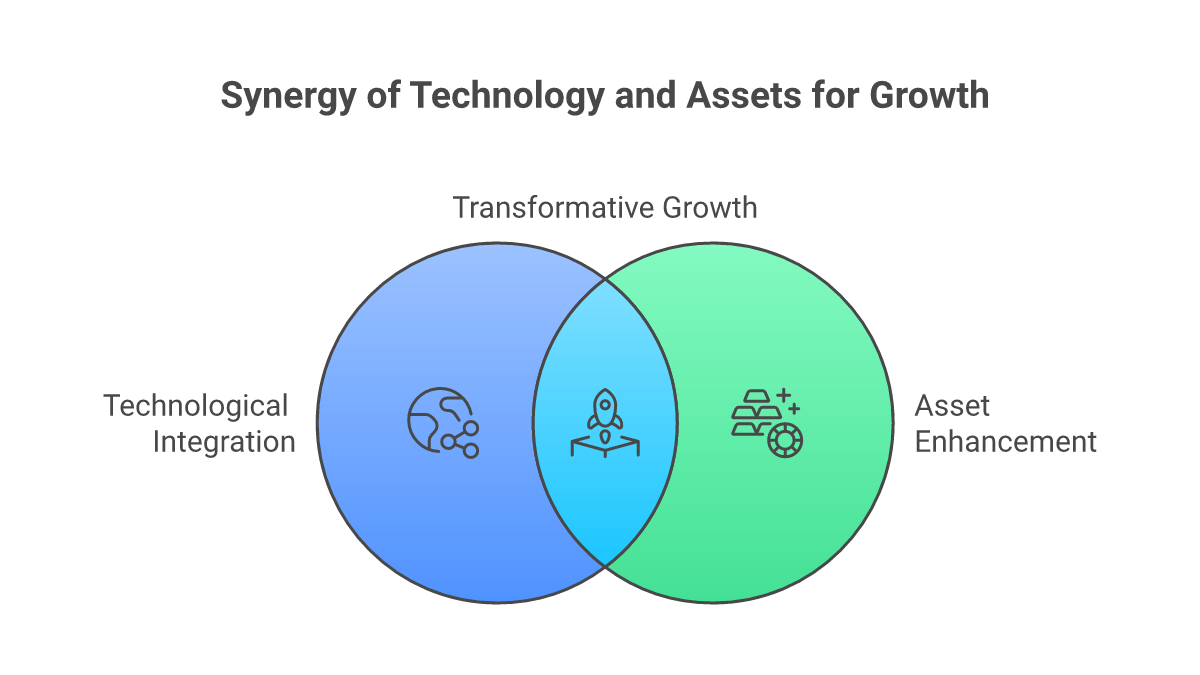

Technological Integration and Asset Enhancement

The gap where technology meets logistics real estate is now quantifiable, with highly automated facilities fetching rental rates 20-30% above the market norm. This premium reflects the growing clout of smart building systems, automated storage setups, and sophisticated warehouse management technology.

Investment in tech infrastructure within logistics properties reached €2.8 billion in 2025, marking a 45% rise since 2024. This injection of capital targets systems that boost operational efficiency, curb energy use, and heighten workforce productivity. Retrofitted facilities with smart lighting systems alone show energy savings averaging between 35% and 45%.

Data analytics capabilities now stand as a key differentiator, with facilities offering cutting-edge monitoring and optimization showing 15% higher tenant retention. The infusion of IoT sensors and real-time analytics empowers operators to fine-tune space use, foresee maintenance needs, and lower operational costs.

Automation readiness is emerging as a pivotal valuation driver, with properties capable of accommodating robotics and automated systems garnering higher premium values. Buildings with clear ceiling heights beyond 12 meters, reinforced floor load capacities, and plentiful power supplies show 25% greater appreciation compared to traditional warehouses.

Sustainability credentials exert growing influence over rent and occupancy stats. Buildings boasting BREEAM Excellence or LEED Gold accolades secure rent premiums of 8-12% and experience 30% less vacancy than their uncertified counterparts.

Future-Proofing Investments in Industrial Real Estate

Research shows that investing in flexible, adaptable buildings yields strong returns. Facilities capable of various configurations offer 40% swifter lease-up times and 15% more rental growth than single-use structures.

Energy efficiency upgrades provide especially convincing returns, with up-to-date energy management systems offering payback periods averaging 3.2 years and internal rate of returns surpassing 25%. In 2025 alone, solar panel installations on logistics facilities surged by 85%, propelled by climbing energy costs and tenant demands for green power.

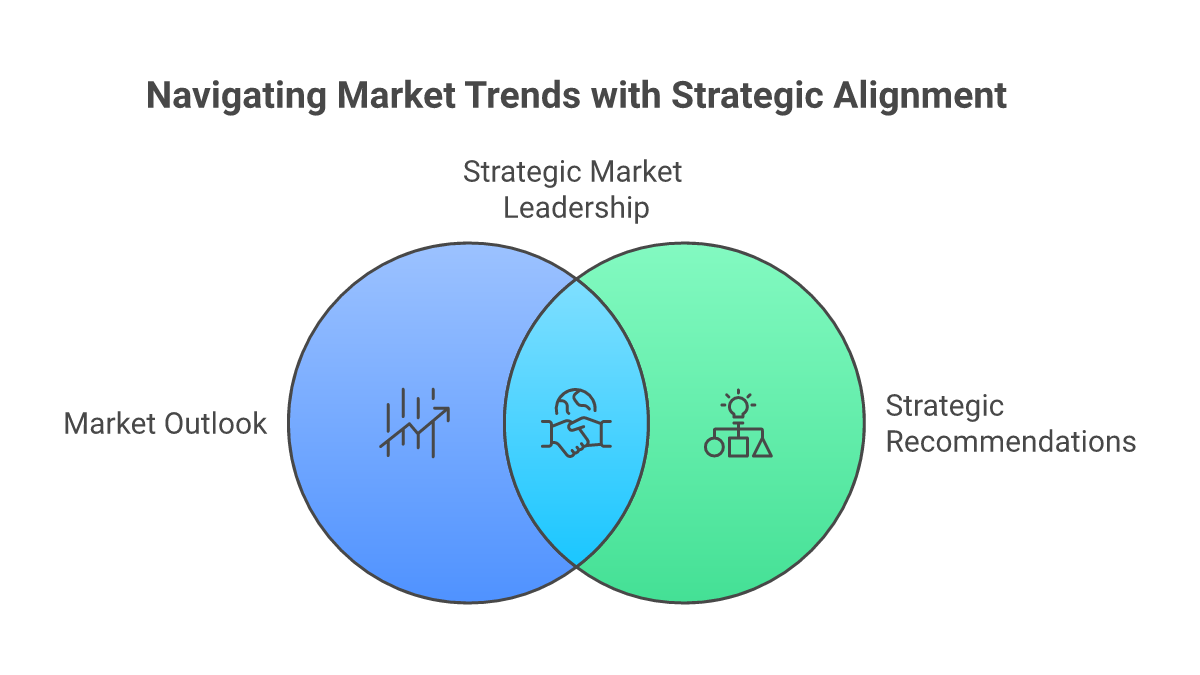

Market Outlook and Strategic Recommendations

The European logistics real estate market is poised to sustain its growth trajectory until 2026, with anticipated investment volumes aiming for €35 billion annually. Prime yields are projected to stabilize around 4.5-5.0% in core markets, while secondary regions might present opportunities for better returns through value-add tactics.

The demand from occupiers remains steadfast, particularly for modern, conveniently located venues with excellent environmental credentials. Projections indicate yearly take-up rates reaching 25 million square meters by 2026, spurred by e-commerce expansion, changes in supply chains, and the rise of third-party logistics providers.

Development activities are predicted to stay sensible, with new supply focusing on established logistics corridors and upcoming hub areas. The pipeline stands at about 4% of the existing stock across Europe, ensuring ongoing rent hikes across most markets.

Environmental, social, and governance (ESG) factors will increasingly sway investment and development choices. Properties meeting top environmental benchmarks are likely to achieve 10-15% higher valuations and face 25% less risk of obsolescence compared to conventional assets.

Labor market trends will continue to shape location strategies, with operators increasingly open to paying premium rents for access to qualified labor pools.

Investment Implications

Core areas still offer steady returns, with prime logistics properties in major distribution centers providing dependable income streams and modest capital growth potential. Value-add opportunities exist in secondary locales where modern, well-specified facilities are in shortage.

Development risks are deemed manageable, given the robust pre-leasing activity and controlled supply channels. Build-to-suit scenarios offer particularly enticing risk-adjusted returns in markets where modern stock is limited.

Conclusion

The European logistics real estate market finds itself at an exciting juncture of growth and technological transformation. With investment volumes hitting €16 billion in the first half of 2025 and rental increases seen across major areas, the market’s core strength is evident. However, attaining success in this changing environment demands more than just conventional real estate acumen.

Players must embrace forward-looking strategies that anticipate changes in supply chain technology, sustainability mandates, and workforce preferences. The most successful will be those able to spot and harness the interplay of location benefits, technological strengths, and environmental performance.

As we look ahead to 2026 and beyond, the future for logistics real estate and commercial warehouse domains seems bright, supported by strong tenant demand, disciplined development activity, and ongoing shifts in retail and distribution models. The key to unlocking this potential lies in understanding and leveraging the market dynamics and strategic insights detailed here.